Debt Recovery vs. Solicitors: Understanding the Difference in the Enforcement Journey

Many believe debt recovery and solicitors are one in the same; however, this isn’t true, and both have their part to play in the process.

Debt recovery is a vital process for any business or individual seeking to reclaim money owed to them. However, the path to reclaiming that debt can vary significantly depending on the method chosen. Two commonly misunderstood approaches in this space are using a debt collection agency versus hiring a solicitor for court proceedings and High Court enforcement. Many believe they are one in the same; however, this isn’t true, and both have their part to play in the process.

While both aim to achieve the same result—getting your money back—they go about it in very different ways. Understanding these differences can save time, money, and unnecessary stress. This article explains what debt collectors can do, why you might prefer one over a solicitor, and when legal intervention is appropriate or even necessary.

What Is Debt Recovery?

Debt recovery refers to the process of pursuing payment of debts owed by individuals or businesses. This can start with simple reminders and escalate all the way to court orders and enforcement action. The method you choose will often depend on factors like:

The size of the debt

The debtor’s responsiveness

The age of the debt

The available documentation

Cost and time considerations

At the outset, many people believe that they need to involve a solicitor straight away. However, that’s not always the most effective—or economical—first step.

Debt Collectors: The First Line of Action

A debt collector, also known as a debt collection agency, is a company that specialises in recovering outstanding debts without necessarily involving the courts. These agencies may be required operate under strict regulations, such as those set out by the Financial Conduct Authority (FCA) in the UK if the debt fits the FCA’s criteria, and focus on negotiation, communication, and resolution.

The main factor to establish if a debt requires an FCA licence to chase are whether the debtor is a consumer entering into a consumer credit agreement. FCA covered debts include:

· Credit and store cards.

· Payday loans.

· Personal loans.

· Overdrafts.

· Mortgages.

· Hire purchase.

· Any other debts covered by the Consumer Credit Act.

Other debts such as invoices, unpaid goods and services and business to business debts do not have the same FCA protection and a debt collector is not required to have an FCA licence to be involved in the chasing of these debts.

What Can Debt Collectors Do?

Contrary to some popular myths, debt collectors cannot:

Enter your home or business without permission

Seize goods

Harass or threaten debtors

But what they can do is:

Contact the debtor via phone, email, post, in person and other methods

Arrange repayment plans

Issue reminders and demands

Mediate communication to resolve disputes

Conduct debtor tracing to find elusive debtors

Negotiate settlements

Their approach is largely about communication, persuasion and persistence rather than “legal” enforcement. Many debts are resolved at this stage without needing to escalate to legal proceedings, which saves both parties time and expense.

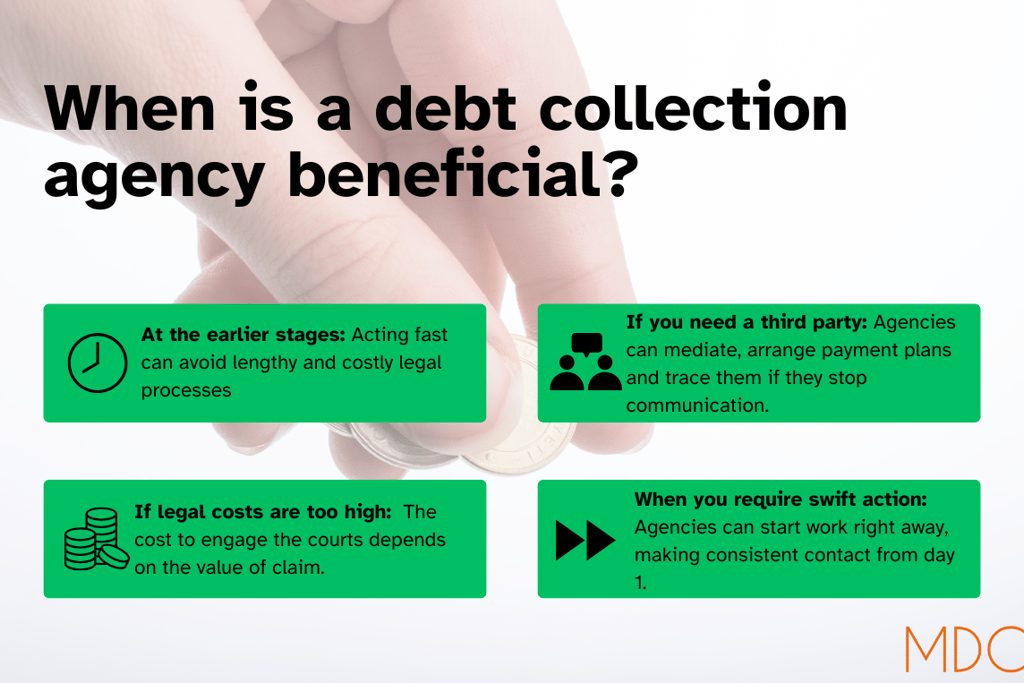

Why Use a Debt Collection Agency?

There are several advantages to using a debt recovery agency instead of going straight to a solicitor:

Lower Cost: Many debt collection agencies work on either an upfront payment, subscription or “no collection, no fee” basis with commission on recovered amounts.

Faster Results: Agencies often have processes in place to act quickly and get the ball rolling immediately.

Expertise in Negotiation: They are trained to deal with debtors and know how to secure payment without creating hostility.

Preservation of Relationships: Where ongoing business relationships matter, debt collectors can act with diplomacy to protect reputations.

In short, a debt collection agency is often the first and most cost-effective step in the debt recovery process

When to Involve a Solicitor

There are cases, however, where a solicitor becomes necessary. If the debtor refuses to pay despite reminders, disputes the debt, or simply disappears, legal proceedings might be a viable option.

Solicitors can:

Issue a Letter Before Action (LBA) – a formal letter warning of legal action

File a claim in the County Court

Obtain a County Court Judgment (CCJ)

Pursue enforcement through the County Court or High Court

This is where debt recovery crosses into legal territory.

The Legal Route: What Happens?

If a CCJ is obtained and remains unpaid, enforcement options include:

County Court bailiffs – Officers employed by the court to collect the debt.

High Court Enforcement Officers (HCEOs) – Used when transferring the case to the High Court for more forceful collection, particularly for debts over £600.

Solicitors handle the paperwork, liaise with the courts, and instruct the relevant enforcement officers when needed.

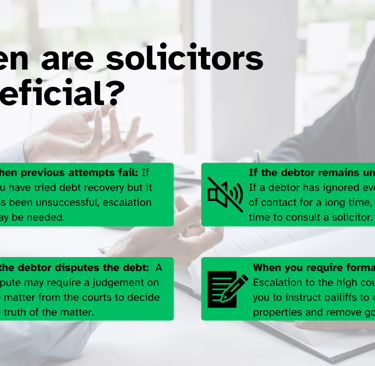

When Should You Use a Solicitor?

Here are some scenarios where involving a solicitor is appropriate:

The debtor is unresponsive or disputing the debt

Previous recovery attempts have failed

The debt amount is high enough to justify legal costs

You need to establish legal liability through a CCJ

You require formal enforcement such as seizure of assets

While solicitors bring authority and legal clout to the process, they can be significantly more expensive. Legal costs may be recoverable if you win your case, but that’s not guaranteed, especially if the debtor has no assets.

The Role of High Court Enforcement

Once a judgment is obtained, especially for debts over £600, many creditors opt to transfer the CCJ to the High Court for enforcement. This enables High Court Enforcement Officers (HCEOs) to act.

What Can HCEOs Do?

HCEOs have more power than standard debt collectors. They can:

Visit a debtor’s property without prior appointment

Seize goods to cover the value of the debt

Enforce court orders quickly and firmly

Solicitors typically handle the transfer-up process to the High Court and liaise with HCEOs on behalf of the creditor.

Debt Recovery: A Step-by-Step Process

Here’s a simplified breakdown of how the debt recovery journey usually works:

Initial Communication – Send your own reminders and invoices.

Use a Debt Collection Agency – Engage professionals for communication, negotiation, and tracing.

Solicitor’s Letter Before Action – If unsuccessful, instruct a solicitor to issue formal demands.

County Court Claim – Solicitor files a claim to obtain a judgment.

Enforcement – If judgment is unpaid, choose County Court bailiffs or High Court enforcement for collection.

At each stage, the cost, likelihood of success, and debtor’s circumstances must be considered carefully

It's About the Right Tool for the Job

Debt recovery and legal enforcement are not interchangeable—they’re parts of a continuum. A debt collector offers an efficient, lower-cost solution that resolves many cases without legal escalation. However, when negotiation fails or legal authority is required, a solicitor steps in to secure judgments and instruct enforcement.

Understanding the differences helps you make informed decisions:

Start with negotiation.

Use debt collectors to avoid unnecessary legal costs.

Bring in solicitors when legal action is essential.

Ultimately, the most effective recovery strategy is one tailored to the situation, using each professional at the right time. Whether you're a small business chasing an unpaid invoice or a landlord recovering rent arrears, knowing how and when to escalate can make all the difference in getting your money back.

Need help choosing between a debt recovery agency or legal route? Let us guide you through the best next step for your situation. Don’t hesitate to reach out for expert advice tailored to your needs.