The Pros and Cons of Different Debt Recovery Options: Choosing the Right Strategy for Your Business

This guide explores the five most common debt recovery options: Upfront Payment Per Debt, No Win, No Fee, Subscription-Based Services, Solicitors and chasing it yourself. We also look into which option is best based on your circumstances.

Debt recovery is an essential, albeit challenging, aspect of running a successful business. Unpaid invoices can severely impact your cash flow, operational efficiency, and overall financial stability. Choosing the right debt recovery strategy is paramount to efficiently reclaiming what's rightfully yours, saving you valuable time and resources.

At McVicar Debt Collection, we pride ourselves on offering professional, ethical, and highly effective recovery solutions, meticulously tailored to your unique business needs. While the market presents various pricing models and promises, discerning the approach that offers the greatest value and minimizes risk is crucial.

This guide explores four common debt recovery options.

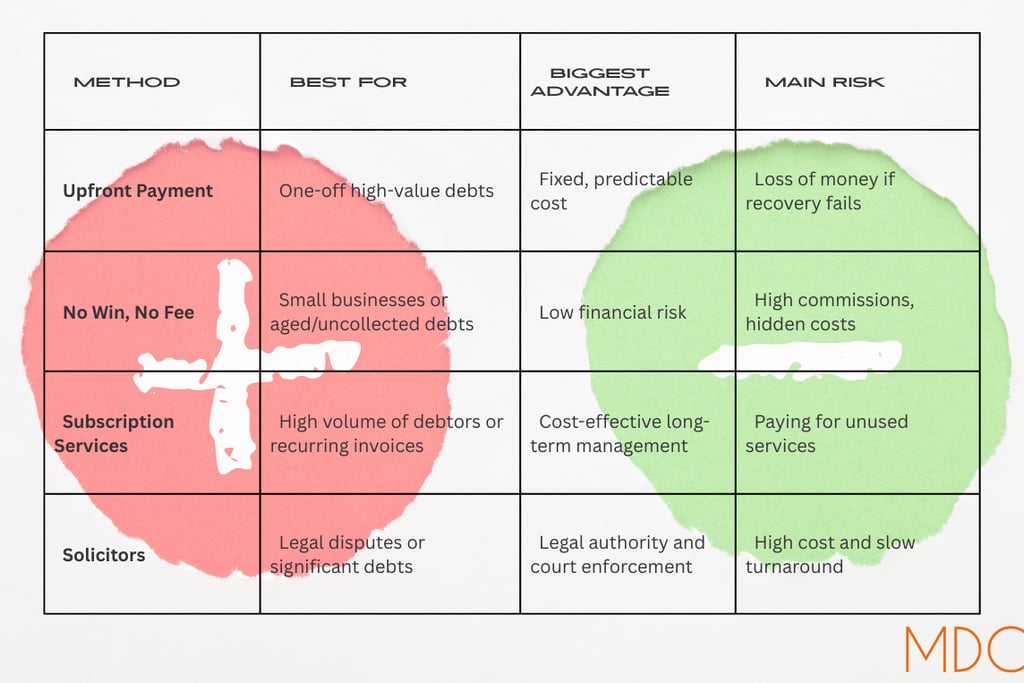

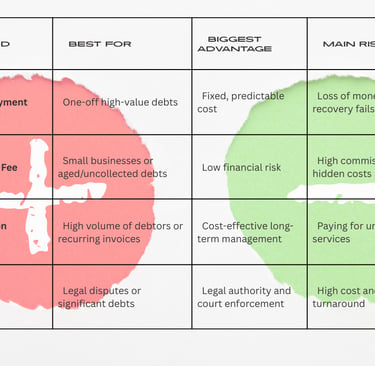

Upfront Payment Per Debt

No Win, No Fee

Subscription-Based Services

Solicitors

Do It Yourself

We will examine the pros and cons of each to help businesses make informed decisions when choosing a recovery method.

1. Upfront Payment Per Debt

What Is It?

This traditional model requires an upfront fixed fee or percentage to pursue a specific debt, regardless of the recovery outcome. Often coupled with a percentage commission upon successful recovery.

Pros for clients:

Predictable Cost Structure: Businesses know in advance what they will be paying, making it easier to budget for. They can weigh up the opportunity cost before signing up.

Motivation for Professional Conduct: Because the agency is paid upfront, they may focus on delivering professional service and protecting their reputation over chasing volume.

Flexible Use: Businesses can use the service on a case-by-case basis, without long-term contracts or commitments.

Pros for the agency:

Initial costs covered: Conducting debt recovery is not free and an up front fee ensures the agency has some form of costs towards at least setting up and running the initial work on a case. It ensures a level of mutual benefit between client and agency.

All debts treated equally: It avoids the need to cherry pick as all clients are ensuring the agency has a level of compensation for putting the work into the case.

Cons:

Cash Flow Impact: For small businesses or companies facing multiple debts, upfront fees can strain budgets without guaranteed return.

Risk of Non-Recovery: You pay even if the debt is not collected. This model doesn’t tie payment to performance and may become a costly gamble with no guaranteed return.

May not be the only fee: Just because you've paid upfront does not mean that is necessarily the only fee you pay. Up front payment agencies may still add a percentage of commission onto money collected or add fees elsewhere such as handling or filing fees to send money onto yourself.

When It Works Best:

This model can suit businesses with a small number of high-value debts or who prefer a one-off, no-commitment approach. However, it carries a level of financial risk if the debt proves unrecoverable.

2. No Win, No Fee

What Is It?

Arguably the most widely promoted option, the “no win, no fee” model means you only pay the collection agency if they successfully recover the debt. Payment is typically a percentage of the amount recovered depending on age, value and complexity of the debt.

Pros:

Low Risk to the Client: There’s no upfront cost, which makes this model particularly appealing for small businesses or those who want to test recovery on older or questionable debts.

Performance-Based: The agency only gets paid if they deliver results, aligning their incentives with yours.

Quick Onboarding: Most “no win, no fee” agencies are ready to start with minimal onboarding, providing fast access to debt recovery efforts.

Pros for the agency:

More debts to chase: Offering no win, no fee means the agency can very easily get more debts onto their system for their teams to chase.

Picking cases: With lots of debts on the books and no risk of financial penalties for not recovering the debt, the agency can choose which debts are most likely to provide success and chase cases that will be the most fruitful.

Cons:

High Commission Rates: Agencies may charge significant percentages for successful collections, especially for older or international debts. Every debt chased must be paid for at some point. With no win no fee, the benefit you get for no upfront fee may mean you are charged a much heavier commission percentage at the back end when successful.

Hidden Charges or Terms: Some agencies advertise “no win, no fee” but add collection fees, legal disbursements, or admin charges that only become clear later. This lack of transparency is common in the industry and can leave clients frustrated.

Cherry-Picking: Agencies may only pursue debts they deem highly recoverable, leaving more complex or aged debts untouched. If your debtor has been evading your for longer or is putting up more of a fight, it does not serve the agency to put more effort into your case when an easier debtor with a larger debt would see them paid more commission and faster.

When It Works Best:

This option suits businesses wanting to reduce financial risk and offload aged or difficult debts. However, success hinges on choosing a reputable agency that offers genuine transparency and ethical practices.

3. Subscription-Based Debt Recovery Services

What Is It?

Under this model, businesses pay a monthly or annual fee to access ongoing debt collection services. This is typically offered by larger debt collection agencies and sometimes bundled with other credit control or invoicing support.

Pros:

Budget Friendly Over Time: For businesses with regular debt occurrences, an annual subscription model offers exceptional value. One payment covers all your historic and future debts within the year, providing cost-effectiveness.

Full-Service Approach: These services often include reporting tools, credit checks, automated reminders, and legal escalation pathways. It is always worth checking with the collection agency to see which features are and aren't offered.

Integrated Collections: You benefit from a cohesive system for managing invoices and arrears, reducing admin and improving cash flow long term.

Pros for the agency:

Access to an evolving portfolio: The collection agency will be bolstered knowing that even if they recover all the current outstanding debts, any debts that become outstanding will be added which secures future work and commission.

Fresh debts: Its no secret a debt is most collectable the earlier it is chased. With a subscription model, the debt is passed the agency at the earliest opportunity meaning it has the highest possible chance of successful recovery.

Cons:

Cost Without Use: If you don’t use the service every month, you’re paying for something that isn’t delivering direct value.

One-Size-Fits-All: Subscription services are typically designed for scalability and may lack the personal touch or tailored strategies of bespoke agencies.

Fixed Terms or Hidden Clauses: If an agency has a monthly subscription model, be cautious of being locked into a fixed term. You don't want to be locked into monthly payments if the volume doesn't suit the length of contract. It may also not be the only fee to be paid, commissions may also still need to be paid on any money recovered.

When It Works Best:

Ideal for businesses with frequent or high volumes of invoices and internal credit control processes that can benefit from automation and scalability. Less suitable for SMEs with only occasional debt collection needs.

4. Solicitors and Legal Action

What Is It?

Hiring a solicitor to pursue debt is very similar to hiring a debt collection agency. Both will start with a simple, pre legal strategy of letters and emails.

Pros:

Legal Weight: A solicitor’s letter can carry significant influence and prompt payment quickly.

Access to Court Options: If the pre legal strategy, solicitors can proceed directly to litigation, judgments, and enforcement.

Authority and Expertise: Complex debts involving contracts, disputes, or cross-jurisdictional issues may benefit from legal analysis and structured escalation.

Cons:

High, often Unpredictable Costs: Solicitors usually charge by the hour, by the letter or with high fixed fees, especially for litigation. This can quickly escalate beyond the value of the debt and you will always need to pay, whatever the outcome.

Slow Process: Legal procedures are rarely fast. Court timelines, procedural delays, and enforcement scheduling can stretch across months.

No Guarantee of Payment: Even with a CCJ in hand, the debtor may still not pay or may be insolvent. Legal action is no guarantee of recovery and you will still need to use some form of enforcement.

Damage to Commercial Relationships: Legal involvement can sour client relationships permanently.

When It Works Best:

Legal action should generally be reserved for larger debts, contractual breaches, or cases where other methods have failed. It’s also appropriate when precedent or deterrence is needed to show you’re serious about non-payment.

5. Do It Yourself

What Is It?

Taking matters into your own hands and chasing the debt yourself. Making the calls, sending the emails, doing the leg work to try and ensure your debtor pays you back.

Pros:

"Free": This method can be done alone and requires no agency input or external company as you are responsible for your own success.

Personal knowledge of the debtor: You and your debtor know each other, you already have a history have had previous contact. If the relationship has not soured, you are on strong footing to resolve it amicably.

Less mess: Stopping the problem by yourself, at source will avoid the need to bring in external agencies or legal entities which will add time, money, stress and financial pressure on both parties.

Cons:

Stops you doing more important tasks: If you do not have a credit control department, you will be pulled from doing what you do best as part of helping your business thrive; developing an opportunity cost of time to recover the debt vs taking care of regular matters.

Lack of legal expertise: Unless you are a qualified Solicitor or have an in house legal team, if a debtor disputes the debt or threatens to launch counter legal proceedings, you may still require advice externally to navigate the situation.

No Guarantee of Payment: You may have a good relationship, you may make regular contact, you may have agreed dates of payment or "waiting until the money comes in" but it could be all talk. Your debtor could be simply trying to take advantage of you.

When It Works Best:

If you have very few debts or a single debt, uncomplicated, undisputed and you have a high level of trust with the debtor, you could attempt to recover the debt yourself first with the thought of employing a debt collection agency should the matter persist beyond a reasonable timeframe. So long as the recovery process is successful and doesn't take too much time away, you can attempt to chase yourself.

Which Debt Recovery Option Empowers Your Business Best?

There is no one-size-fits-all approach to debt recovery. The best method will depend on your industry, average invoice size, frequency of unpaid debts, and your appetite for risk and investment.

Here’s a quick comparison table to help:

Ready to take control of your outstanding debts and secure your financial future?

Debt recovery is more than chasing money—it’s about safeguarding your cash flow, protecting your business, and upholding financial fairness. While “no win, no fee” offers low entry risk, it must be scrutinized. Upfront payments can work if managed wisely, subscription services offer scale, and solicitors have their place in more complex scenarios.

Whatever your choice, always prioritize working with a professional, trustworthy agency that aligns with your business values.

Need help with outstanding debts?

Get in touch with McVicar Debt Collection today for a free, non-biased consultation about which option would be best for yourself. Once your case has been assessed, you can select a method that suits you. you can do so either by clicking the button below, by calling 01772 584507 or by rmailing newbusiness@mcvicardebtcollections.co.uk